📊 What is time series decomposition and why should you know it if you work with data?

Time series are everywhere: monthly sales, energy consumption, market quotes, web traffic…

When we analyze a time series, often it’s not enough to look at raw values. We need to understand its internal structure.

That’s where time series decomposition comes in.

🔍 What is it?

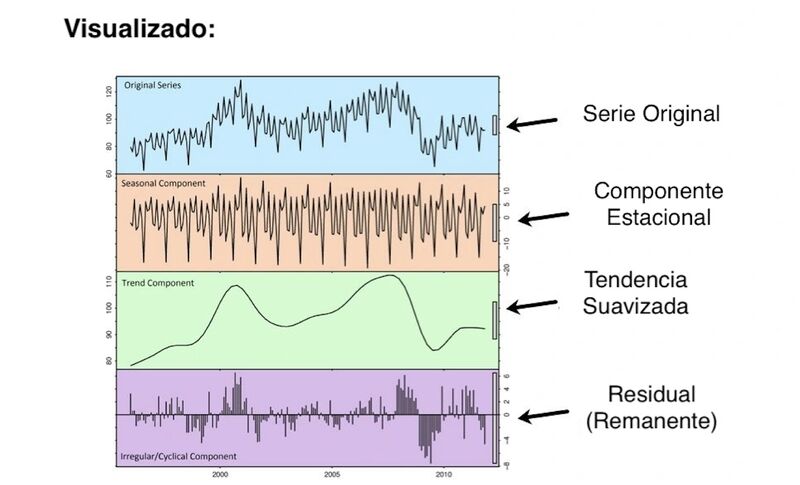

Decomposition separates a series into three key components:

- Trend: the general long-term direction.

- Seasonality: regular cyclic patterns (for example, yearly or monthly seasonality).

- Noise (residual): what cannot be explained by the other two.

🧪 How to do it with Python? With just a few lines of code using statsmodels:

import pandas as pd

from statsmodels.tsa.seasonal import seasonal_decompose

import matplotlib.pyplot as plt

# Load your time series

df = pd.read_csv("sales.csv", parse_dates=["date"], index_col="date")

series = df["sales"]

# Decompose

decomposition = seasonal_decompose(series, model='additive', period=12)

# Visualize

decomposition.plot()

plt.show()🧠 This technique lets you answer questions like:

- Are we growing despite seasonal fluctuations?

- What part of the variability is predictable?

- When is a value truly an “anomaly”?

💡 Ideal for improving forecasting models, better understanding your business, or detecting unusual behavior.

Also published on LinkedIn.